The squeezed middle. Everyone knows what it is. Challenged from above and particularly below, dire predictions were made about the death of the mid-market gym, which have happily proved untrue. The sector has survived, has adapted and – although some say there’s more pain to come before the corner is finally turned – the general consensus is that, while low-cost gyms may be here to stay, this does not mean the mid-market gym is an endangered species.

This process is typical of so many markets. A new proposition is lauded as a market game changer, grows rapidly as it’s adopted, and then hits a plateau and it becomes another player.

Consider TV: we’re too young to remember when this new kid on the block was going to kill off radio. Or more recently e-books: it was reported recently that electronic book sales declined slightly last year. And what about digital radio, which was predicted to wipe out analogue services? (This may still happen, but it will be driven by government demand rather than simple market forces.) Or vinyl records: I’ve lost count of the times I’ve been told recently that this medium, so much warmer and realistic than CD and electronic versions, is recovering. Sales of turntables, as well as vinyl, are growing.

Sure, there are also examples where products and services have died a death: cassette tapes, floppy disks, VHS tapes, video hire shops to name a few. These have generally been replaced because something came along that could do exactly the same thing, only better and often cheaper. Television can’t do everything that radio can. Readers have come to value the physical book, unless perhaps it’s one they don’t want to be seen holding on their commute. There’s something special about holding a vinyl LP.

Benefits that ensure survival and growth can be emotional or functional. Unless it’s a direct replacement, price is only one element of the marketing mix – and this is as true for the gym market as it is for every other one.

Effective segmentation

In fact, the mid-market is a pretty good place to be – if you get it right. It’s clear at the moment that low-cost offerings are popular, but these tend to thrive when times are hard and incumbents have taken their eye off the ball: while Aldi and Lidl are currently driving the grocery market, a key reason for this is that the mainstream mid-market operators were complacent. They failed to give their customers good reasons to keep using them, and they failed to spot significant changes in shopping behaviour.

There’s almost certainly going to be consolidation before things turn around, but it would be a brave pundit who forecasts the death of the grocery mid-market. The leading players have woken up and are reviewing, re-configuring and re-presenting themselves so they have a distinct positioning in the new landscape. Sound familiar?

So how does a mid-market gym operator get it right? We’re constantly told we need to differentiate, to create a clear space that’s easily understood, and to stick to it. We can – and should – do this by understanding the neighbourhood where the gym sits, by listening to members (not forgetting leavers, to understand why they didn’t want to stay), by understanding their emotional as well as their physical needs, and by investing in the right equipment, facilities and staff. And by charging the right price for that differentiated offer.

There’s only point in differentiating if it’s in ways that are meaningful to the customer. A large pub company I know which has 750 pubs does this successfully. It has six core brands, ranging from gastro pubs through traditional locals, city centre and sports pubs to family-orientated offers where provision is made for the kids to let off steam. Each pub is assigned to a brand according to the location, what the customers there want, and what they’re most likely to buy.

Customers in all markets are driven by a range of factors which – depending on the individual member’s characteristics – are ‘dialled up or down’. We all know the person who’s driven by value, or convenience, or personal service and so on. Price is obviously another of these factors, but with gyms, other factors are likely to include staff numbers, staff attentiveness and expertise, sophistication of equipment, amount and range of equipment, size of premises, facilities, classes, information, support, ‘extra curricular’ activities and changing facilities (size, style etc).

Some of these will be hygiene factors – what you have to offer just to get into the consideration set – and some will be real differentiators. An effective segmentation will let you determine which factors are more important to the different member types, and which are real deal-breakers for them.

Predictably irrational

But while research can place relative values on each of these factors, we can’t ask people directly what these factors are as none of us, from a rational point of view, actually think that way. People don’t use rational criteria to buy goods, services or memberships.

Dan Ariely’s excellent book Predictably Irrational gives countless examples of ways we can be manipulated to buy what the seller wants us to buy and how, in his words, we don’t actually know what our preferences are. We’re not rational beings who consider all the implications of the choices we make. This is why segmentation and differentiation is a tricky business: direct questions will yield direct answers which are over-rationalised and often bear no relation to reality.

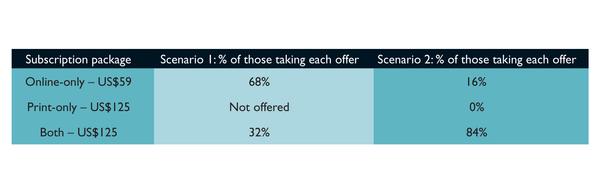

One of Ariely’s favourite examples concerns subscription charges for The Economist. Two scenarios were tested among different groups: the first offered an online subscription for US$59 and a print + online subscription for US$125, while the second offered these two plus a print-only subscription, also at US$125. Table 1 shows the choices respondents made in the two scenarios.

When offered, the print-only subscription gets no buyers, so it’s an apparently useless offer. Yet its presence has a significant effect on the choices buyers actually make. Offer this ‘useless’ option and five in six will trade up and buy the bundle. Remove it as an individual option and the proportion of people who buy the bundle falls to two in six. That’s a loss of US$66 for every potential subscriber who chooses the online-only option. Put another way, for every 100 subscribers, the presence of an option that’s never actually purchased means The Economist would take an additional US$3,432. It’s clear the seller can, to an extent, affect the choices we make by controlling the environment in which we make those choices.

User-friendly pricing

It’s better to be as simple and clear as possible with price. Have a finite number of options and don’t keep changing them. Create bundles that contain mixes of the important factors for your market, in ways that are easily understood. See if your mother could easily work out which rate she would like to be on, and whether you can – realistically – justify all elements.

Joining fees could come into this bracket: how do you justify them? Does it cover an induction? If so, all well and good, but if it’s for pressing a few buttons on the keyboard it will be harder to keep in place.

One option might be higher value bundles that allow people to move across services and sites through their membership period – eg drop the pool as I’m not using it, add sauna as I benefit from that, take a multi-site membership for a month as I’m moving around (and let me do that from the place I’ve come to as well as from my regular gym).

And don’t necessarily drop an option just because nobody buys it – this could be the key package that trades members into higher value options.