SELECTED

ISSUE

SELECTED

ISSUE

|

|

Leisure Management - Profit & Loss

Ask an expert

|

|

| Profit & Loss

|

The viability of some spas is being undermined by unreasonable expense allocations, highlights a session at the Global Spa & Wellness Summit

Katie Barnes, Spa Business

|

Hotel spa operators are often asked to cover pool and gym costs with no benefit to their bottom line shutterstock.com/Goodluz

Contributors to the investor panel, led by Harmsworth (left), debated whether a uniform P&L measure for spas is the answer

|

|

|

“I’ve been in the spa industry for over 40 years and I’ve seen an increasing disconnect in the financial expectations of hotel owners, investors and operators and spa operators,” said Susan Harmsworth, owner of ESPA International who moderated an Investor Panel session at this year’s Global Spa & Wellness Summit (GSWS) in New Delhi (see p70). “Even those at the top of their game don’t understand the numbers, which can make attracting investors or funding for new spas difficult,” she added. A big confusion is the expectation of return on investment – how long should it take for a spa to break even? Often projections by spa operators, which have the facility running at a loss for the first year as the business beds in, don’t marry up to expectations of hotel owners, investors and operators who want to start making money as quickly as possible. Moreover, in hotel spas there’s a fundamental problem with predicting return on investment with regards to allocation of initial capital expenditure (capex). It’s left too late in the build before the cost of a spa is considered and ROI is defined. Harmsworth explains: “In the past, I’ve been asked to run the pool and gym [as part of the spa business], but bundling these costs into the profit and loss (P&L) of a spa makes it look unviable, because the pool and gym capex and operational expenses (opex) should really be with the hotel. This becomes particularly problematic when hotel’s prohibit spa/health club membership which can help cover costs. There are no industry norms and it’s making it extremely difficult for spa operators – whether run by a third-party or the hotel itself – to be profitable in certain markets.” Is it time for the industry to take a stand on this? Or is there a way of cross charging the pool and gym and other expenses to the hotel so that the figures stack up? There’s an argument that a spa can contribute more to a hotel business than merely what’s seen on the P&L account. They can be a powerful tool in branding, PR and market differentiation, as well as helping to boost room rate, secondary spend and leisure business – drawing in double occupancy – during off peak/season periods. But how can spa operators convince hoteliers and potential investors and owners that this is the case? Of course, hotel spas aren’t the only model in the industry, so how do standalone day spas, mixed-use/residential spas or destinations spas compare in terms of viability? Harmsworth herself answers these queries along with hospitality consultants Omer Isvan and Manav Thadani who joined her in the GSWS session, and operators Andrew Gibson and Talal Bin Ali who put forward questions from the audience.

|

|

|

Susan Harmsworth

Founder & CEO

ESPA International

|

|

What we do as spa operators is typically not understood by hotel owners or operators, especially those in emerging countries. And sometimes their own expectations are misaligned with each other. The owner, understandably, doesn’t want the spa or hotel to make a loss in the first year, yet the hotel operator doesn’t want to give the spa any revenue.

At the same time, we get loaded with operating costs including marketing and the pool and gym. Sometimes even when a spa does soak up the costs of a pool and gym, the hotel operator doesn’t give it credit. And that’s regardless of whether the spa is operated by a third-party company or managed in-house.

If a spa can offer outside membership, it can use that extra revenue to cover costs, but if a hotel wants to keep use exclusive to its guests it’s difficult for a spa to then cover additional cleaning, laundry and energy expenses. Cross charging could be the answer. I’ve got a residential tower, hotel and spa with minimal space so I’ve suggested to the operator that we don’t include a pool. When he insisted that a pool is necessary for the selling of the residential tower, I reasoned that that’s where the capex should be allocated rather than to the spa.

In another example, we have a spa being built in a mixed-use development that’s exclusively used by residents and isn’t open to the public. As the spa is a communal facility, all the costs are included in the service charge of residents. Plus we’re taking a fixed annual management fee because there’s no external [membership or day spa] business so we can’t influence profit.

Looking at stand-alone day spas, with their own capex and opex it’s clear that the business can work – my very first spa in 1970 was a stand-alone. But they’re usually driven by individuals and are difficult to roll out.

The hotel spa industry has changed because since the economic downturn, everything has become so bottom-line driven. It’s not necessarily a bad thing to pay more attention to the financials, but this exacerbates the need for spas and hotel owners and operators to agree early enough what ROI is expected, over what period and what constitutes capex and opex. What’s fair will differ in every case – I think spas should be paying a percentage of costs but they shouldn’t be paying it all and there needs to be room for negotiation. Unfortunately, until a standard is developed for spa P&L, consistency in sector benchmarking will also remain problematic.

In addition, there’s a need to show the other added benefits a spa has above and beyond P&L. We’ve got several city hotels that are full of single occupancy business guests Monday to Thursday and they would be quiet at the weekend if it wasn’t for the spa that’s driving double occupancy leisure guests – sometimes up to 30-40 per cent occupancy – on a Friday, Saturday and Sunday.”

Looking forwards, the industry needs to fight its corner more to get P&Ls loaded in the right way. It needs to start fighting early enough to get a fair agreement that works for both parties and ultimately the guest – because if you don’t have integrated businesses they’re the ones who will suffer too.”

GSWS board member Susan Harmsworth has a portfolio of more than 350 spas worldwide.

Details: www.espaonline.com

What’s fair will differ in every case – I think hotel spas should be paying a percentage of capex and opex costs but they shouldn’t be paying it all and there needs to be room for negotiation

|

|

|

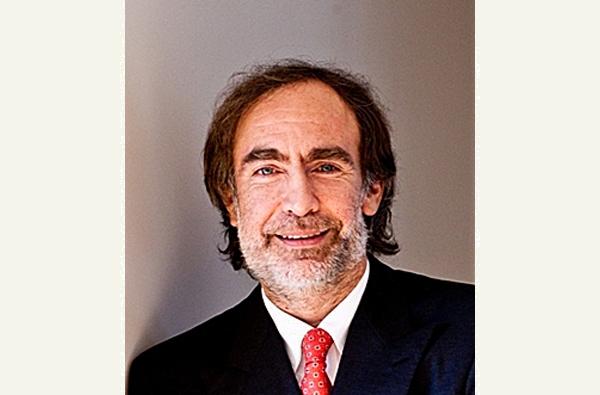

Omer Isvan

President

Servotel Corporation

|

|

Return expectations for spas vary greatly depending on who’s investing in what market. When a company from an emerged market invests in an already developed market, it’s driven by debt coverage ratio, asset yield and the value payback period with a focus on exit value and the internal rate of return.

Where does the spa feature in a new investment? Beyond allocating some space, it doesn’t feature until much later in the game unless the right people are on board from the outset. It’s often seen either as an investment burden as it costs so much per square metre; or, at best, seen as a good tool to utilise otherwise valueless basement floors.

When a company from an emerging market invests in a developing market it comes down to ROE – or return on ego! The numbers become secondary to what the spa should look and feel like. After a three-year honeymoon period, however, they start to measure profitability and that’s when the gym, pool and even the outdoor pool get bundled into the same P&L so the spa can look like a loss leader.

Hotels use a uniform system of accounts where undistributed operating expenses like heat, lighting, water and maintenance are – rightly or wrongly – shared across departments, including the spa. If this happens to a hotel’s own-branded spa it’s not such a problem, as many mainstream hotel spas are viewed as a managed function rather than a major profit centre. But when a third-party spa operator comes in, expectations are raised, expenses are scrutinised and they’re often lumbered with a lot of the otherwise undistributed opex. All of a sudden, new meters get installed, measuring how much energy or water the spa uses.

It’s easy to suggest that hoteliers should consider the intrinsic advantages of having a spa, but there’s not always a mathematical formula on what it can yield indirectly. Sometimes a spa can become a central conceptual element, but that would take sophisticated planning which isn’t happening (as yet) when left to the cut and paste mainstream hotel brands. I know some successful destination spas where this is the case, but substantial wellness elements haven’t come into play in mixed-use developments or mainstream hotels at any scale.

We’re not specialists in small scale stand-alone urban spas, but from my observation the successful ones are ‘person-centric’ – meaning there’s one person or specialist around which the establishment has formed and where their skill-set meets a niche market.

Servotel has offices in Istanbul and London. Isvan has worked in hospitality for 27 years.

Details: www.servotel.net

It’s easy to suggest that hoteliers should consider the intrinsic advantages of having a spa, but there’s not always a mathematical formula on what it can yield indirectly

|

|

|

Manav Thadani

Chairman

HVS South Asia

|

|

It’s true that ROI expectations for a spa depend on the type of investor. It’s the ego-driven investor that spas really want because they’re less concerned about the amount of money that’s going in or the time frame. They only want the best.

Another fundamental difference is that the bigger, mainstream hotels don’t look at spas as big revenue generators – at best they represent 3-4 per cent of the overall revenue. So they’re given a lot less importance.

I don’t look at a spa in terms of yield and the investment. I look at it in terms of how much space it’s going to take up and whether that space could be used for meetings, F&B or additional rooms so I can generate more revenue. But that’s in the mainstream. If it’s a luxury hotel and a spa can add 10-15 per cent on my room rate then I might look at that.

But it also depends on the market. In an urban location where real estate is more expensive (especially in India) I’d favour more bedrooms as it’s less hassle and it will bring more to the bottom line. But if I was looking at a leisure destination, then I’d definitely focus on the spa to sell rooms.

Mixed-use and residential facilities with spas are very different. When the spa is exclusively for that development and not open to the public, viability becomes an issue – we have to look at striking a balance between what fixed cost we can charge residents and at what point we introduce a pay per use fee.

On the other hand, standalone day spas can work extremely well. In India they typically generate 35-45 per cent profit. Personally, I wouldn’t like to visit them as they’re in noisy malls, but they’re definitely attracting customers. Would I lease or rent out a space to day spas in a hotel? Most certainly yes. We have properties with vacant space that we’d love to lease out to a spa that’s complementary to our services. In this part of the world, a spa focused on express treatments would work really well.

However, if spa operators want to convince mainstream hotels to look at their business more favourably, I think benchmarking is needed. It would certainly help with recognition because right now those details aren’t there.

Over the past 15 years, Thadani has worked on 800 hospitality projects across India for HVS South Asia.

Details: www.hvs.com

|

|

|

Andrew Gibson

Group director of spa

Mandarin Oriental Hotel Group

|

|

The confusion surrounding ROI is created if there’s a lack of clarity or a misalignment of expectations. In my opinion, ROI should be judged on the entire hotel/resort business model where each part – rooms, restaurants, spas, pools, fitness, meeting rooms, public spaces – combine to make it work. The current method of trying to separate these parts is flawed because there’s no consensus on allocation of costs.

It’s fine if the capex of a pool and gym is undertaken [by the spa] for a reason that’s been considered and approved by the investor. But if the capital costs are subdivided to create individual business centres then the revenues and returns on those centres should get allocated too.

The leisure facilities of a hotel are often viewed as loss leaders because the business model is incorrectly determined. Research body STR has estimated the premium on the room rate for luxury hotels – ie those with all the extra leisure facilities – in the US is around US$76 (€55, £47). If this premium was added into the ROI for the pool, fitness and spa then a more realistic figure might be obtained. Our own internal research at Mandarin Oriental has also shown that guests using the spa contribute almost double spend on food and beverage, stay longer and are more likely to book a suite. Perhaps this should also be included in ROI calculations? As you can see, once the model gets broken into individual segments, the true allocation of returns becomes difficult. It is for this reason that there’s confusion.

The simple solution is not to break down the ROI any more than you would try to determine the ROI on the lobby of a hotel or a piece of artwork in a corridor.

That said, spa operators – in the absence of industry benchmarks and figures – should still gather their own research and data to show how much value their operations have. The evaluations of spas from hotel investment advisors are generally poor at best and misleading at worst. The link between spas and hotel guestroom premiums, increased spend in outlets, attraction to the hotel, local community usage of hotel services and direct P&L returns are good financial indicators. Publicity, awards and editorial coverage provide intangible returns that should also be used in arguments for a spa. In my opinion the argument for a spa in a four- or five-star hotel is already won based on the needs to obtain the star rating so the key question is what size is effective to yield the expected return on investment.

Gibson oversees 24 spas at Mandarin Oriental, is a GSWS board member and was a co-chair for this year’s summit.

Details: www.mandarinoriental.com

Our own internal research has shown that guests using the spa contribute almost double spend on food and beverage, stay longer and are more likely to book a suite. Perhaps this should also be included in ROI calculations?

|

|

|

Talal Bin Ali

Founder & president

Enaya Care International

|

|

If the spa industry is to flourish, we must present our businesses in a different light. We need to convince the hospitality sector that they’re sustainable, valuable and viable models even if the spas are run as standalone enterprises within their sites.

On the other hand, hotels also need to view spas as a more important amenity like F&B. We’ve been approached by hotels owners who want us run our businesses from their premises but we’ve rejected these offers, as they view spas as a side dish rather than a main course!

We currently have 12 standalone beauty salons and day spas under the Enaya brand in Jeddah, Saudi Arabia; as well as 10 Cutzone barber shops. Typically, an Enaya salon or spa will cover 600sq m (6,458sq ft) and have 25 treatment rooms where beauty/maintenance services, as well as mind and body treatments will be offered.

On average, our salons and spas generate a minimum 50 per cent gross profit after staff and material costs. They’re managed as independent profit centres and we make sure they’re viable through cost control and smart pricing, including loyalty schemes, promotions, discounts and alliances with other businesses to attract more people – the higher the utilisation, the higher the profit.

We’ve managed to secure funding because we have the figures to prove we’ve got good top line growth (over 25 per cent annually), that we’re profitable and that our financing matches the payback period. I’d advise any operator who’s looking to attract investment to be just as cost conscious and to measure and manage key performance indicators with a good software system.

If our industry is to overcome the confusion surrounding profitability and ROI we must be proactive. Having a spa attracts customers to a hotel and increases occupancy rates, so spas should be assessing what the occupancy of a hotel is – with and without a spa – what footfall it creates and what impact it has on other profit indicators to prove how valuable spa facilities really are.

Following a 20 year career working for companies such as Unilever, Talal Bin Ali started the Enaya chain in 2006. He plans to roll out the brand in Saudi Arabia and the gulf states in the next five years. Details: www.enayacare.com

|

|

|

| Originally published in Spa Business 2013 issue 4

|

|

|

|